DXC Technology Reports Fourth Quarter Fiscal Year 2022 Results

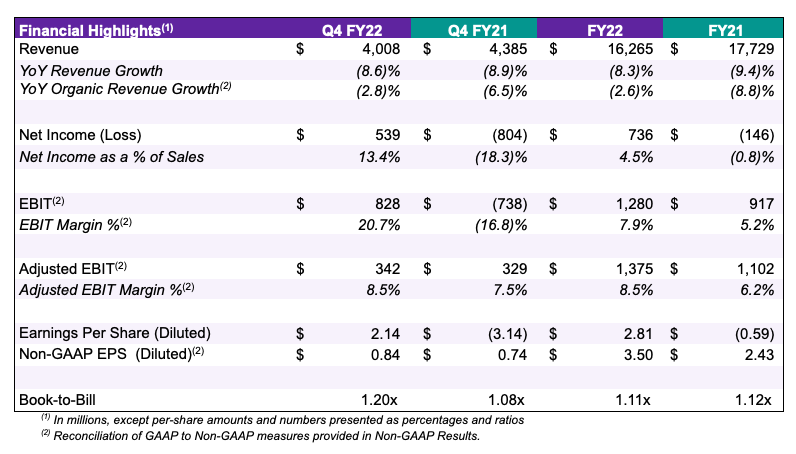

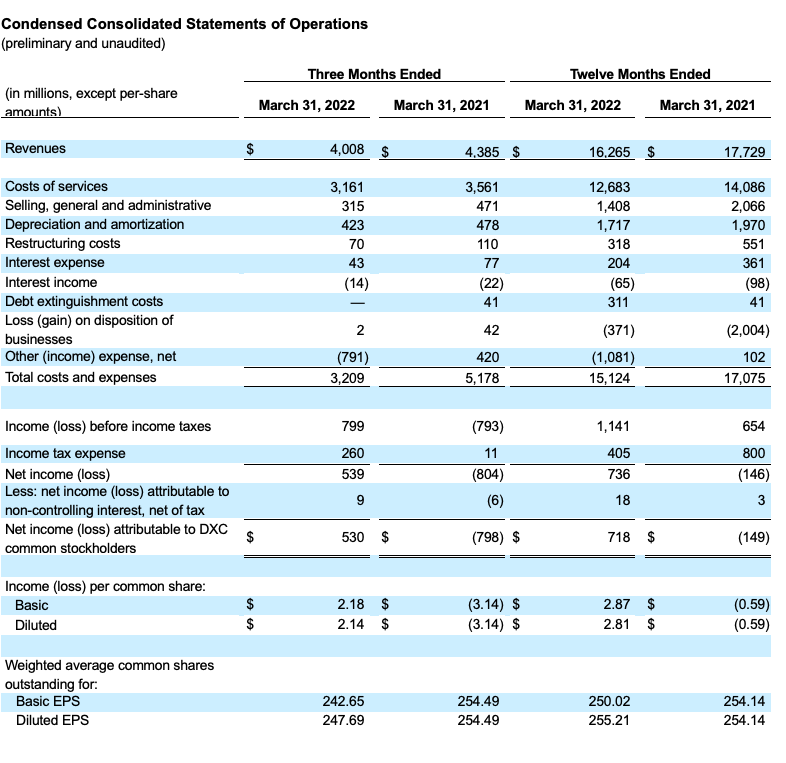

- Revenues of $4.01 billion for Q4 FY22, down 8.6% as compared to prior year period, and down 2.8% on an organic basis

- Diluted Earnings Per Share was $2.14 and Non-GAAP Diluted Earnings Per Share was $0.84 in Q4 FY22

- Bookings of $4.8 billion and book-to-bill ratio of 1.20x in Q4 FY22

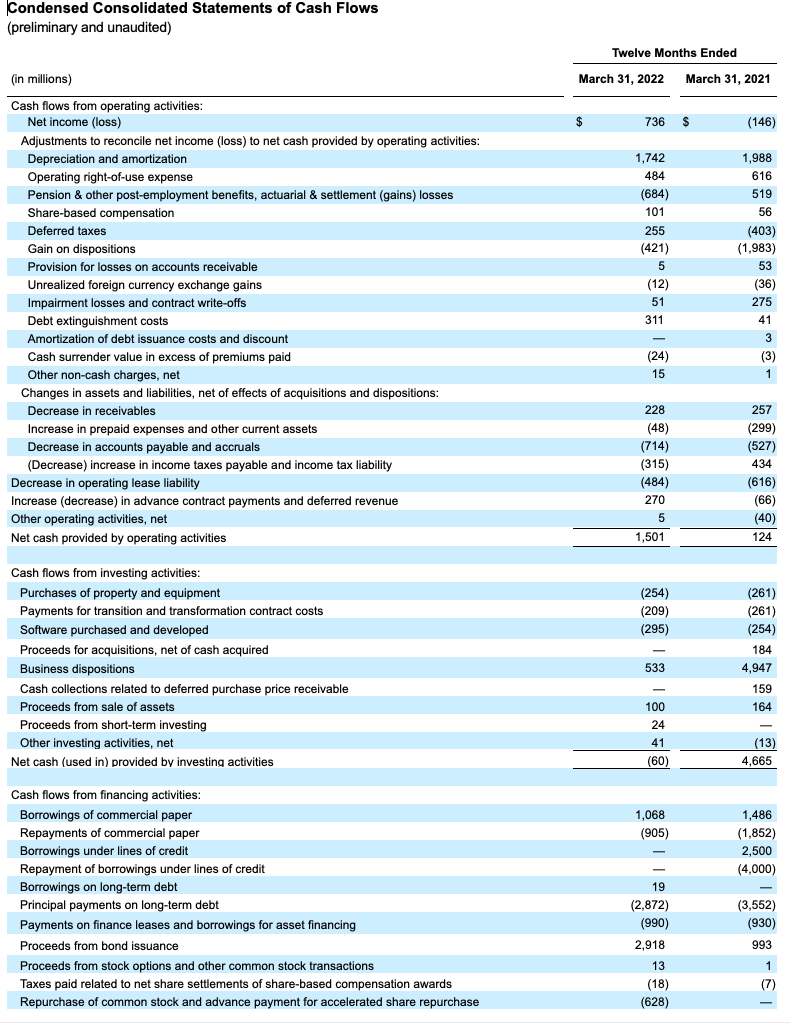

- FY22 operating cash flow of $1,501 million, less capital expenditures of $758 million, results in $743 million of free cash flow, a $1.4 billion improvement over FY21

- Returned $271 million to shareholders by repurchasing 8.2 million shares in Q4 FY22, bringing FY22 repurchases to $634 million or 18.8 million shares. Repurchased over 7% of shares outstanding in FY22

ASHBURN, Va., May 25, 2022 — DXC Technology (NYSE: DXC) today reported results for the fourth quarter and full fiscal year 2022.

“I would like to thank our DXC colleagues across the organization for coming together to deliver excellence for our customers and colleagues in the midst of the challenges raised by the ongoing conflict in Ukraine," said Mike Salvino, DXC President and Chief Executive Officer. “Our transformation journey starts with our people, and we are honored by the commitment, dedication, and caring we have seen from our people in the region and throughout the company over the past few months.”

Mr. Salvino continued, "DXC is now in a dramatically better place and I am pleased with the ongoing business momentum that DXC has achieved in FY22. We significantly improved our organic revenue performance, expanded margins, drove strong Adjusted EPS growth, and improved free cash flow by $1.4 billion as compared to FY21. I am excited about FY23 and the clarity that our leadership team has as to what we need to execute within GBS and GIS in order to meet our long-term targets.”

Financial Highlights - Fourth Quarter of Fiscal Year 2022

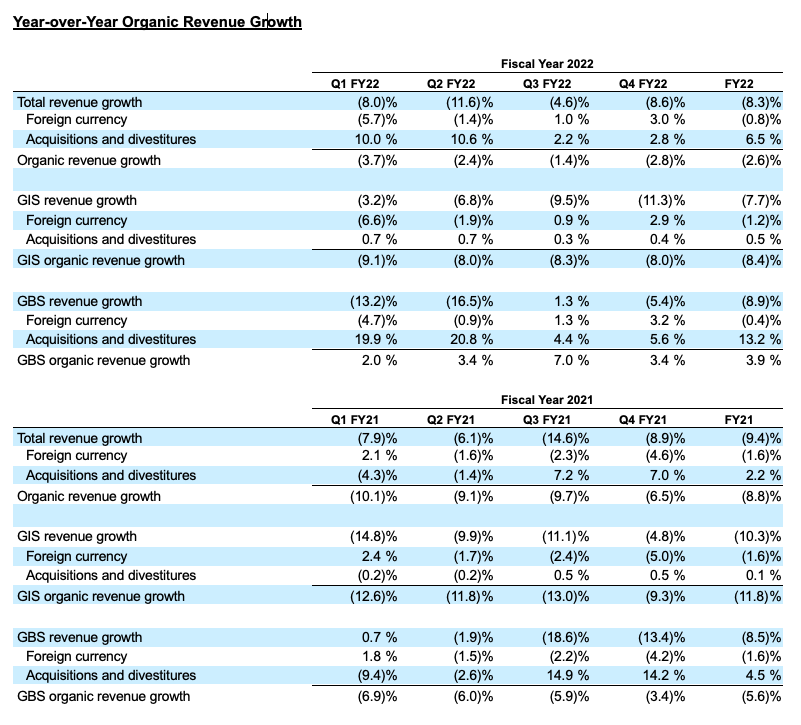

Revenue was $4.01 billion for the fourth quarter of fiscal year 2022, down 8.6% as compared to prior year period, and down 2.8% on an organic basis. Fourth quarter revenues came in below the previous guidance range, as the strengthening of the U.S. dollar reduced fourth quarter fiscal year 2022 revenues by $52 million as compared to the currency rates used in our prior earnings guidance. Management estimates that Russia's invasion of Ukraine, exiting our Russian business, and the associated distraction accounted for the majority of the organic revenue miss to guidance.

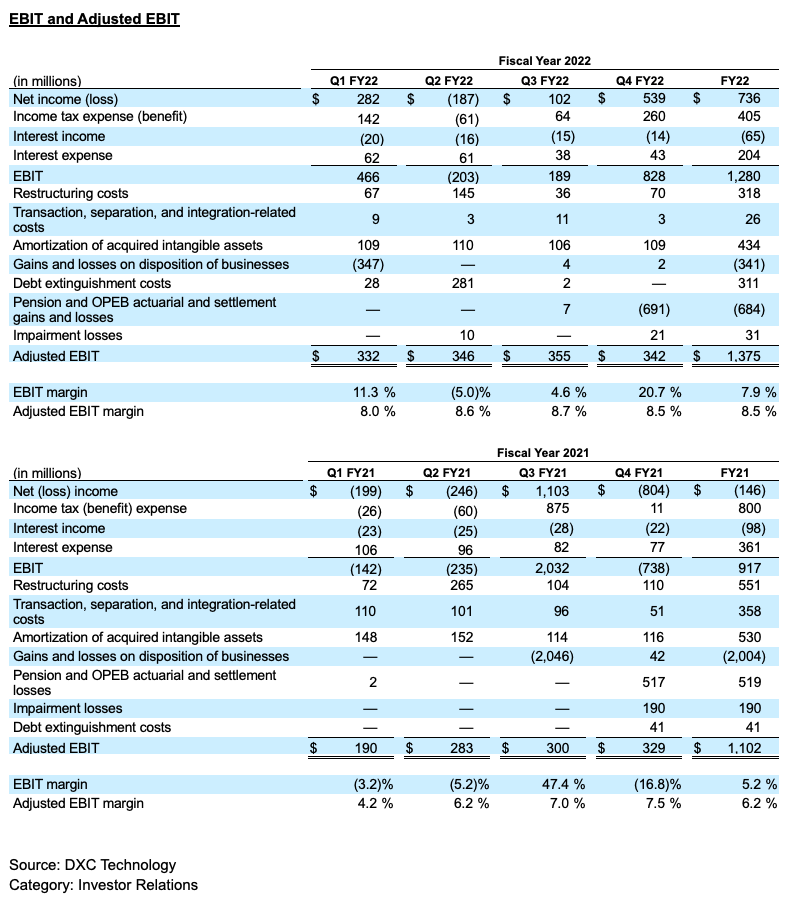

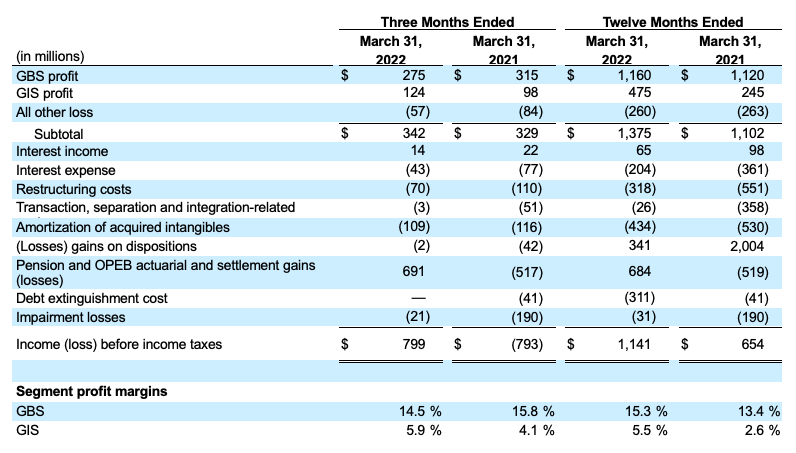

Net income was $539 million, or 13.4% of sales for the fourth quarter of fiscal year 2022, compared to $(804) million, or (18.3)% of sales, in the prior year quarter. EBIT was $828 million or 20.7% of sales. Net income and EBIT in the quarter included the following items: amortization of acquired intangible assets of $109 million, restructuring costs of $70 million, mark-to-market pension gain of $691 million, loss on disposition of $2 million, asset impairment loss of $21 million, and transaction, separation, and integration costs of $3 million. Excluding these items, Adjusted EBIT margin was 8.5% in the fourth quarter, an improvement of 100 bps as compared to the prior year quarter. Fourth quarter adjusted EBIT margin was reduced by $16 million of expenses, or 40 basis points, related to Russia's invasion of Ukraine.

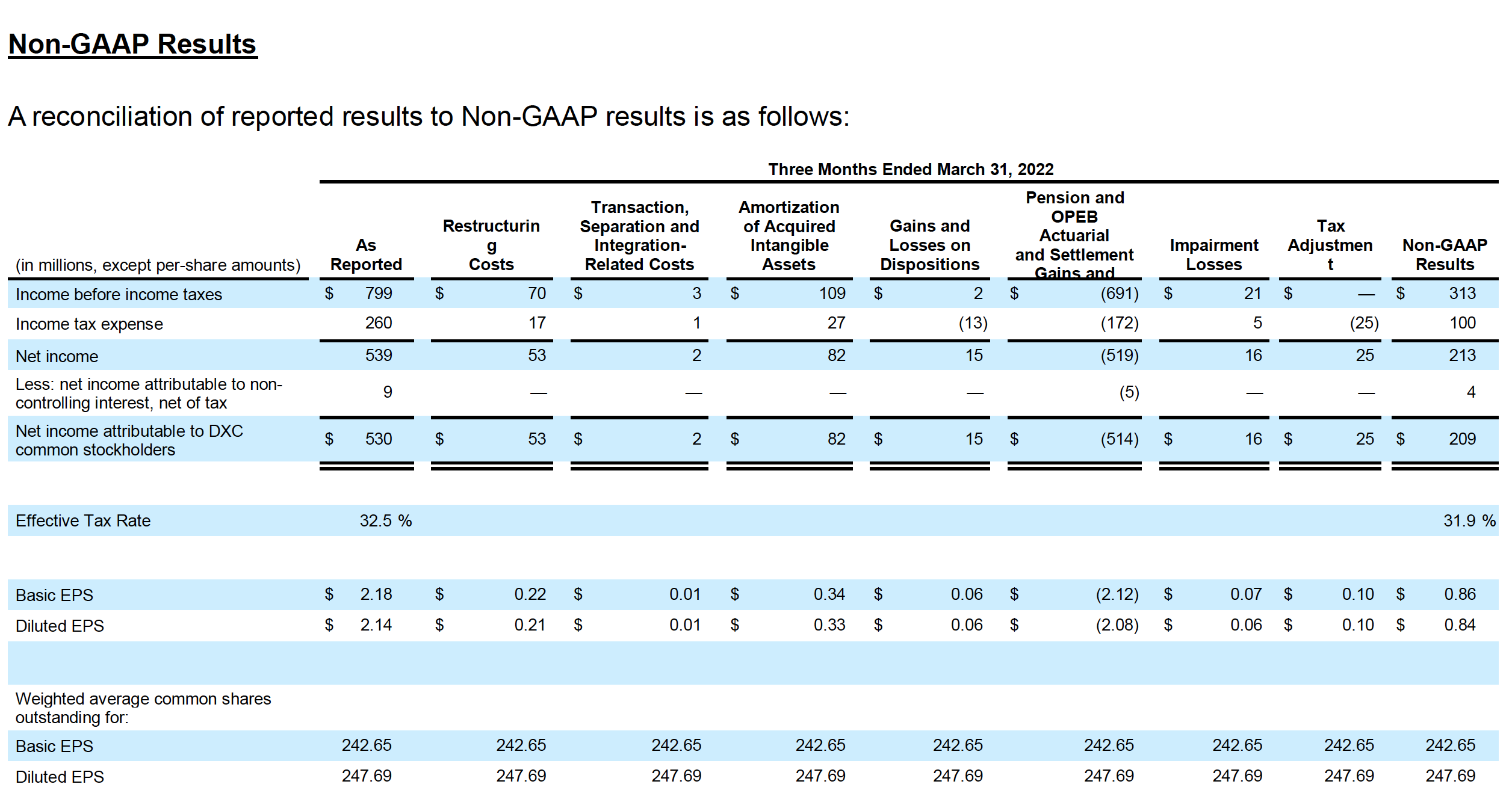

Diluted earnings per share was $2.14 and Non-GAAP diluted earnings per share was $0.84 for the fourth quarter of fiscal year 2022, driven by the improvement in margins, lower interest expense, and lower shares outstanding. Non-GAAP earnings per share fell below the Company's previous guidance range due to $0.04 per share of incremental costs related to Russia's invasion of Ukraine, $0.07 of headwinds related to higher than expected tax expense due to the write down of a deferred tax asset, and an incremental $0.06 in higher European energy costs that we were not able to pass on to customers.

Book-to-bill for the quarter was 1.20x. Over the trailing four quarters, the company delivered a book to bill of 1.11x.

During the fourth quarter, the Company repurchased 8.2 million shares of common stock for a total of $271 million. For the full fiscal year 2022, the company repurchased 18.8 million shares for a total of $634 million.

Ukraine / Russia Update

Subsequent to the end of the quarter, DXC exited its domestic Russian business. This action achieves a significant portion of our commitment to exit Russia. The sale of this business has provided continuing employment opportunities for many former DXC employees who have chosen to stay in Russia. The exit of this market will reduce revenues by approximately $140 million annually. The company is transitioning global business previously serviced by our DXC Russian colleagues to international teams and expects to complete this process by the end of the second quarter.

DXC's Ukraine business supported approximately $250 million of revenue, predominantly serving international customers. Despite the ongoing conflict, these revenues have only seen a minor impact stemming from the conflict. Our global teams have worked to augment their Ukrainian colleagues, and to continue to deliver for our customers through the conflict.

During the fourth quarter, DXC spent approximately $16 million related to Russia's invasion of Ukraine.

Financial Information by Segment

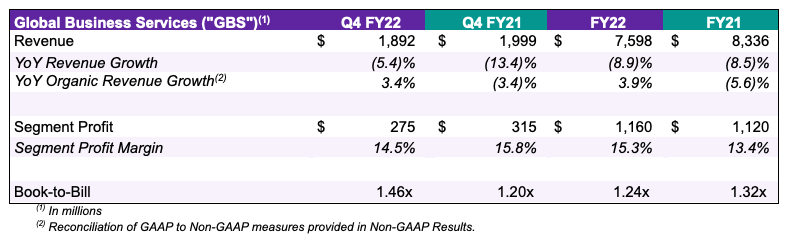

GBS segment revenue was $1,892 million in the fourth quarter of fiscal year 2022, down 5.4% compared to prior year period and up 3.4% on an organic basis. The GBS performance was driven by strong growth in the Analytics & Engineering business, where revenue increased 19.7% on an organic basis. GBS segment profit was $275 million and segment profit margin was 14.5%, down 130 bps compared to prior year, primarily due to expenses related to Russia's invasion of Ukraine. GBS bookings for the quarter were $2.8 billion for a book-to-bill of 1.46x.

GBS segment revenue was $1,892 million in the fourth quarter of fiscal year 2022, down 5.4% compared to prior year period and up 3.4% on an organic basis. The GBS performance was driven by strong growth in the Analytics & Engineering business, where revenue increased 19.7% on an organic basis. GBS segment profit was $275 million and segment profit margin was 14.5%, down 130 bps compared to prior year, primarily due to expenses related to Russia's invasion of Ukraine. GBS bookings for the quarter were $2.8 billion for a book-to-bill of 1.46x.

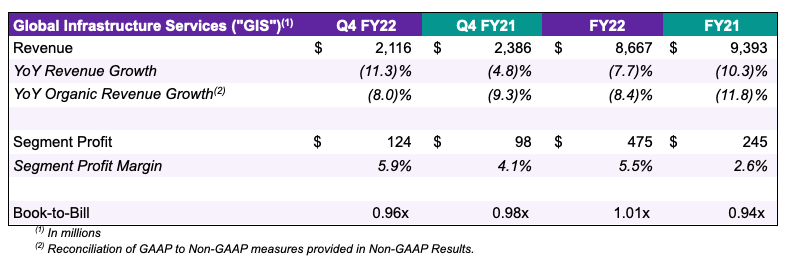

GIS segment revenue was $2,116 million in the fourth quarter of fiscal year 2022, down 11.3% compared to prior year period, and down 8.0% on an organic basis. GIS segment performance was driven by improving Cloud and Security revenues, which declined by 6.9% on an organic basis, offset by lower resale revenues in Modern Workplace. GIS segment profit was $124 million with a segment profit margin of 5.9%, a 180 bps margin expansion as compared to fourth quarter of fiscal year 2021. GIS bookings were $2.0 billion in the quarter for a book-to-bill of 0.96x.

Enterprise Technology Stack Highlights

The components of the Enterprise Technology Stack are as follows:

Cash Flow

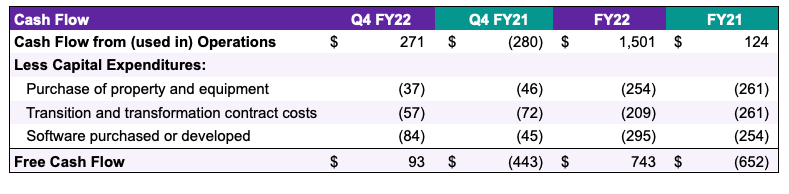

Cash flow from (used in) operations was $271 million in the fourth quarter of fiscal year 2022, as compared to $(280) million in the fourth quarter of fiscal year 2021, and capital expenditures were $178 million in the fourth quarter of fiscal year 2022, as compared to $163 million in the fourth quarter of fiscal year 2021. Free cash flow (cash flow from operations, less capital expenditures) was $93 million in the fourth quarter of fiscal year 2022, as compared to $(443) million in the fourth quarter of fiscal year 2021.

Guidance

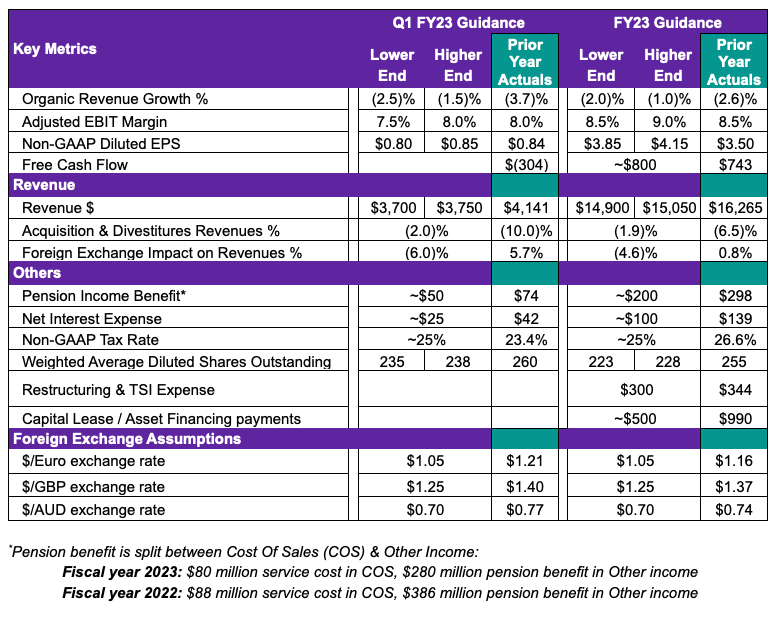

The Company's guidance for the first quarter and full fiscal year 2023 is as follows:

The Company reaffirmed its longer-term guidance:

- Positive organic revenue growth of 1% to 3% for fiscal year 2024

- Adjusted EBIT margin of 10% to 11% in fiscal year 2024

- Non-GAAP diluted Earnings Per Share of $5.00 to $5.25 in fiscal year 2024

- Free cash flow of approximately $1.5 billion in fiscal year 2024

- Restructuring and TSI of approximately $100 million in fiscal year 2024

DXC does not provide a reconciliation of Non-GAAP measures that it discusses as part of its guidance because certain significant information required for such reconciliation is not available without unreasonable efforts or at all, including, most notably, the impact of significant non-recurring items. Without this information, DXC does not believe that a reconciliation would be meaningful.

Ken Sharp, Chief Financial Officer, commented: “In FY22, we made excellent progress in building our financial foundation. We significantly lowered our debt and related interest expense, substantially reduced restructuring, transaction, separation and integration expenses, and lowered capital expenditures, capital lease originations and our facility footprint. These initiatives, and the ongoing strong business execution of our DXC colleagues, allowed us to deliver a $1.4 billion improvement in free cash flow over FY21. We continue to execute on our capital deployment program, repurchasing 18.8 million shares during the year, and expect to complete our $1 billion repurchase commitment over the next three quarters. We look forward to the opportunities presented by FY23 and expect to continue our steady progress on the transformation journey."

Earnings Conference Call and Webcast

DXC Technology senior management will host a conference call and webcast to discuss these results on May 25, 2022, at 5:00 p.m. EDT. The dial-in number for domestic callers is +1 (888) 330-2455. Callers who reside outside of the United States should dial +1 (240) 789-2717. The passcode for all participants is 4164760. The webcast audio and any presentation slides will be available on DXC Technology’s Investor Relations website.

A replay of the conference call will be available from approximately two hours after the conclusion of the call until June 1, 2022. Phone number for the replay is +1 (800) 770-2030 or +1 (647) 362-9199. The replay passcode is 4164760.

About DXC Technology

DXC Technology (NYSE: DXC) helps global companies run their mission critical systems and operations while modernizing IT, optimizing data architectures, and ensuring security and scalability across public, private, and hybrid clouds. The world’s largest companies and public sector organizations trust DXC to deploy services across the Enterprise Technology Stack to drive new levels of performance, competitiveness, and customer experience. Learn more about how we deliver excellence for our customers and colleagues at DXC.com.

Forward Looking Statements

All statements in this press release that do not directly and exclusively relate to historical facts constitute “forward-looking statements.” Forward-looking statements often include words such as “anticipates,” “believes,” “estimates,” “expects,” “forecast,” “goal,” “intends,” “objective,” “plans,” “projects,” “strategy,” “target,” and “will” and words and terms of similar substance in discussions of future operating or financial performance. Forward-looking statements include, among other things, statements with respect to our future financial condition, results of operations, cash flows, business strategies, operating efficiencies or synergies, divestitures, competitive position, growth opportunities, share repurchases, dividend payments, plans and objectives of management and other matters.

These statements represent current expectations and beliefs, and no assurance can be given that the results described in such statements will be achieved. Such statements are subject to numerous assumptions, risks, uncertainties and other factors that could cause actual results to differ materially from those described in such statements, many of which are outside of our control. Furthermore, many of these risks and uncertainties are currently amplified by and may continue to be amplified by or may, in the future, be amplified by, the ongoing coronavirus disease 2019 (“COVID-19”) pandemic and the impact of varying private and governmental responses that affect our customers, employees, vendors and the economies and communities where they operate. Important factors that could cause actual results to differ materially from those described in forward-looking statements include, but are not limited to: the uncertainty of the magnitude, duration, geographic reach of the COVID-19 crisis, its impact on the global economy and the impact of current and potential travel restrictions, stay-at-home orders, vaccine mandates and economic restrictions implemented to address the crisis; our inability to succeed in our strategic objectives; the risk of liability or damage to our reputation resulting from security incidents, including breaches, and cyber-attacks to our systems and networks and those of our business partners, insider threats, disclosure of sensitive data or failure to comply with data protection laws and regulations in a rapidly evolving regulatory environment, in each case, whether deliberate or accidental; our inability to develop and expand our service offerings to address emerging business demands and technological trends, including our inability to sell differentiated services up the Enterprise Technology Stack; our inability to compete in certain markets and expand our capacity in certain offshore locations and risks associated with such offshore locations such as Russia’s recent invasion of Ukraine and our exit from the Russian market; failure to maintain our credit rating and ability to manage working capital, refinance and raise additional capital for future needs; our indebtedness; the competitive pressures faced by our business; our inability to accurately estimate the cost of services, and the completion timeline of contracts; execution risks by us and our suppliers, customers, and partners; the risks associated with natural disasters; our inability to retain and hire key personnel and maintain relationships with key partners; the risks associated with prolonged periods of inflation; the risks associated with our international operations, such as risks related to currency exchange rates and Brexit; our inability to comply with governmental regulations or the adoption of new laws or regulations, including social and environmental responsibility regulations, policies and provisions; our inability to achieve the expected benefits of our restructuring plans; inadvertent infringement of third-party intellectual property rights or our inability to protect our own intellectual property assets; our inability to procure third-party licenses required for the operation of our products and service offerings; risks associated with disruption of our supply chain; our inability to maintain effective internal control over financial reporting; potential losses due to asset impairment charges; our inability to pay dividends or repurchase shares of our common stock; pending investigations, claims and disputes and any adverse impact on our profitability and liquidity; disruptions in the credit markets, including disruptions that reduce our customers’ access to credit and increase the costs to our customers of obtaining credit; our failure to bid on projects effectively; financial difficulties of our customers and our inability to collect receivables; our inability to maintain and grow our customer relationships over time and to comply with customer contracts or government contracting regulations or requirements; our inability to succeed in our strategic transactions; changes in tax laws and any adverse impact on our effective tax rate; risks following the merger of Computer Sciences Corporation and Enterprise Services business of Hewlett Packard Enterprise Company's businesses, including anticipated tax treatment, unforeseen liabilities and future capital expenditures; and risks following the spin-off of our former U.S. Public Sector business and its related mergers with Vencore Holding Corp. and KeyPoint Government Solutions in June 2018 to form Perspecta Inc., which was acquired by Peraton in May 2021. For a written description of these factors, see the section titled “Risk Factors” in DXC’s Annual Report on Form 10-K for the fiscal year ended March 31, 2021, and any updating information in subsequent SEC filings, including DXC’s upcoming Annual Report on Form 10-K for the quarterly period ended March 31, 2022.

No assurance can be given that any goal or plan set forth in any forward-looking statement can or will be achieved, and readers are cautioned not to place undue reliance on such statements which speak only as of the date they are made. We do not undertake any obligation to update or release any revisions to any forward-looking statement or to report any events or circumstances after the date of this press release or to reflect the occurrence of unanticipated events except as required by law.

About Non-GAAP Measures

In an effort to provide investors with supplemental financial information, in addition to the preliminary and unaudited financial information presented on a GAAP basis, we have also disclosed in this press release preliminary Non-GAAP information including: earnings before interest and taxes ("EBIT"), EBIT margin, Adjusted EBIT, Adjusted EBIT margin, Non-GAAP diluted EPS, organic revenues, organic revenue growth, and free cash flow.

We believe EBIT, EBIT margin, Adjusted EBIT, Adjusted EBIT margin, and Non-GAAP diluted EPS provide investors with useful supplemental information about our operating performance after excluding certain categories of expenses. Free cash flow represents cash flow from operations, less capital expenditures.

One category of expenses excluded from Adjusted EBIT, Adjusted EBIT margin, and Non-GAAP diluted EPS, incremental amortization of intangible assets acquired through business combinations, may result in a significant difference in period over period amortization expense on a GAAP basis. We exclude amortization of certain acquired intangible assets as these non-cash amounts are inconsistent in amount and frequency and are significantly impacted by the timing and/or size of acquisitions. Although DXC management excludes amortization of acquired intangible assets primarily customer-related intangible assets, from its Non-GAAP expenses, we believe that it is important for investors to understand that such intangible assets were recorded as part of purchase accounting and support revenue generation. Any future transactions may result in a change to the acquired intangible asset balances and associated amortization expense.

Another category of expenses excluded from Adjusted EBIT, Adjusted EBIT margin, and Non-GAAP diluted EPS, impairment losses, may result in a significant difference in period over period expense on a GAAP basis. We exclude impairment losses as these non-cash amounts, reflect generally an acceleration of what would be multiple periods of expense and do not expect to occur frequently. Further assets such as goodwill may be significantly impacted by market conditions outside of management’s control.

We believe organic revenue growth provides investors with useful supplemental information about our revenues after excluding the effect of currency exchange rate fluctuations for currencies other than U.S. dollars and the effects of acquisitions and divestitures in the periods presented. See below for a description of the methodology we use to present organic revenues.

Selected references are made to revenue growth on an “organic basis” so that certain financial results can be viewed without the impact of fluctuations in foreign currency rates and without the impacts of acquisitions and divestitures from “organic basis” financial results, thereby providing comparisons of operating performance from period to period of the business that we have owned during all periods presented. Organic revenue growth is calculated by dividing the year-over-year change in GAAP revenues attributed to organic growth by the GAAP revenues reported in the prior comparable period. This approach is used for all results where the functional currency is not the U.S. dollar.

There are limitations to the use of the Non-GAAP financial measures presented in this press release. One of the limitations is that they do not reflect complete financial results. We compensate for this limitation by providing a reconciliation between our Non-GAAP financial measures and the respective most directly comparable financial measure calculated and presented in accordance with GAAP. Additionally, other companies, including companies in our industry, may calculate Non-GAAP financial measures differently than we do, limiting the usefulness of those measures for comparative purposes between companies.

Segment Profit

We define segment profit as segment revenues less costs of services, segment selling, general and administrative, depreciation and amortization, and other income (excluding the movement in foreign currency exchange rates on our foreign currency denominated assets and liabilities and the related economic hedges). The Company does not allocate to its segments certain operating expenses managed at the corporate level. These unallocated costs include certain corporate function costs, stock-based compensation expense, pension and other post-retirement benefits (“OPEB”) actuarial and settlement gains and losses, restructuring costs, transaction, separation and integration-related costs, and amortization of acquired intangible assets.

Reconciliation of Non-GAAP Financial Measures

Our Non-GAAP adjustments include:

- Restructuring costs – includes costs, net of reversals, related to workforce and real estate optimization and other similar charges.

- Transaction, separation and integration-related (“TSI”) costs – includes costs related to integration, planning, financing and advisory fees and other similar charges associated with mergers, acquisitions, strategic investments, joint ventures, and dispositions and other similar transactions.(1)

- Amortization of acquired intangible assets – includes amortization of intangible assets acquired through business combinations.

- Gains and losses on dispositions – gains and losses related to dispositions of businesses, strategic assets and interests in less than wholly-owned entities.(2)

- Impairment losses – impairment losses on assets classified as long-term on the balance sheet.(3)

- Debt extinguishment costs – costs associated with early retirement, redemption, repayment or repurchase of debt and debt-like items including any breakage, make-whole premium, prepayment penalty or similar costs as well as solicitation and other legal and advisory expenses.(4)

- Pension and OPEB actuarial and settlement gains and losses – pension and OPEB actuarial mark to market adjustments and settlement gains and losses.

- Tax adjustments – reflects discrete tax adjustments to impair or recognize certain deferred tax assets and adjustments for changes in tax legislation. Income tax expense of merger and divestitures is separately computed based on the underlying transaction. Income tax expense of all other (non-discrete) non-GAAP adjustments is computed by applying the jurisdictional tax rate to the pre-tax adjustments on a jurisdictional basis.(5)

(1) TSI-Related Costs for all periods presented include fees and other internal and external expenses associated with legal, accounting, consulting, due diligence, investment banking advisory, and other services, as well as financing fees, retention incentives, and resolution of transaction related claims in connection with, or resulting from, exploring or executing potential acquisitions, dispositions and strategic investments, whether or not announced or consummated.

The TSI-Related Costs for the fourth quarter of fiscal 2022 include $1 million of costs to execute HHS and HPS dispositions and $2 million of costs incurred in connection with activities related to other acquisitions and divestitures.

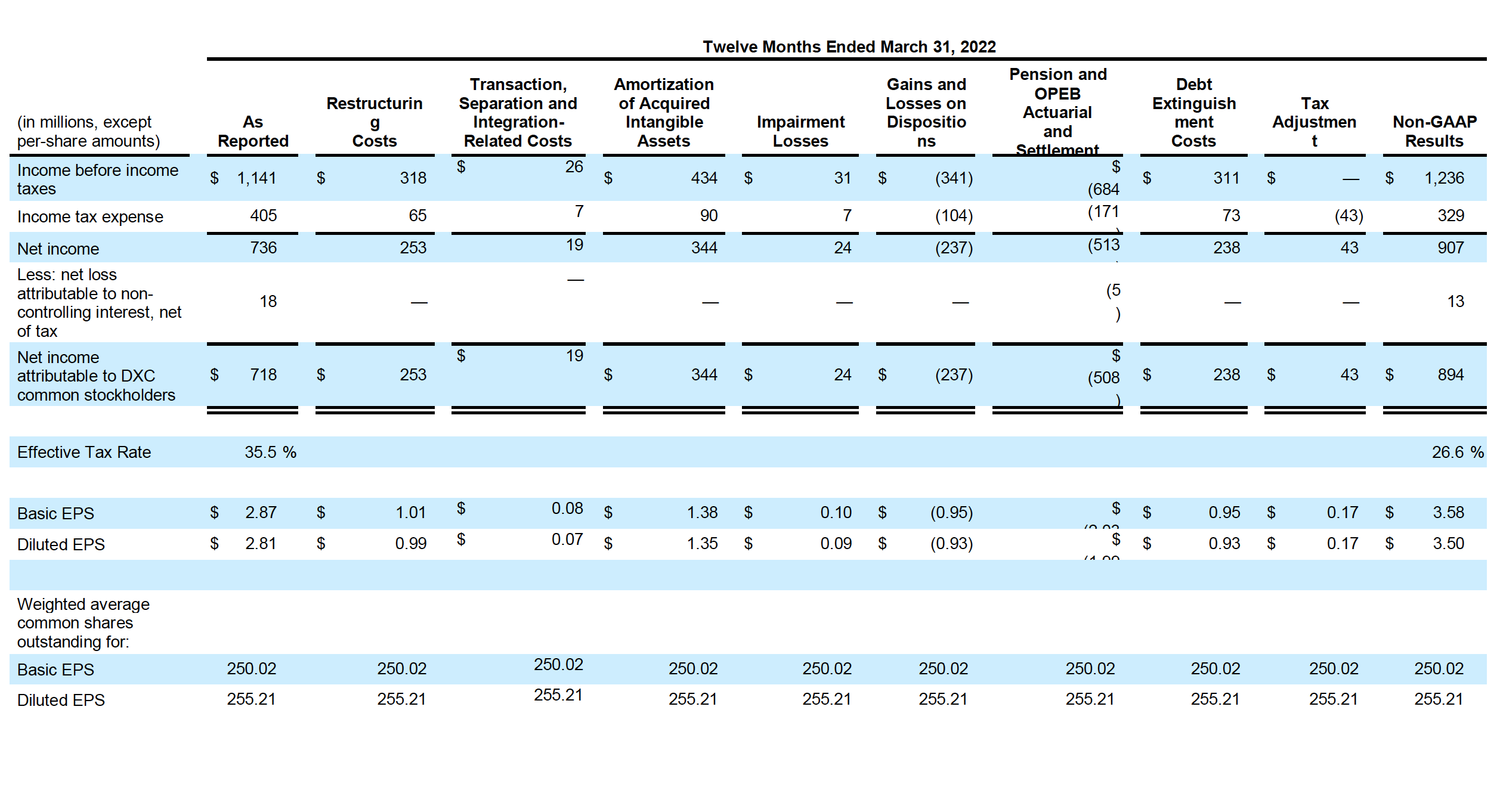

The TSI-Related costs for fiscal 2022 include $14 million of costs to execute dispositions (including $2 million for the sale of HHS which closed in October 2020 and $12 million for the sale of HPS which closed on April 1, 2021); $2 million legal costs and a ($12 million) credit towards Perspecta Arbitration settlement; $5 million in expenses related to integration projects resulting from the CSC – HPE ES merger (including costs associated with continuing efforts to separate certain IT systems) and $17 million of costs incurred in connection with activities related to other acquisitions and divestitures.

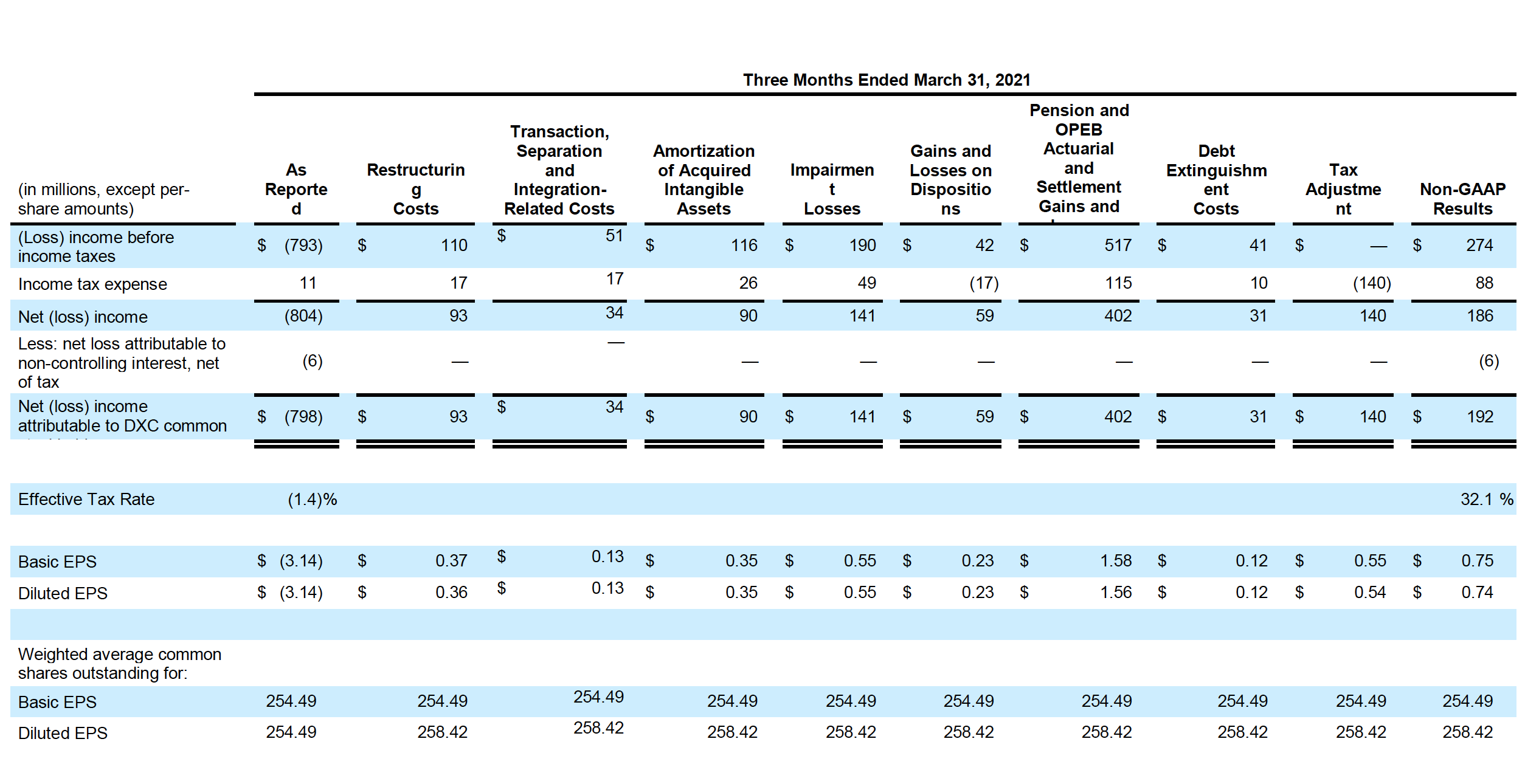

The TSI-Related Costs for the fourth quarter of fiscal 2021 include $25 million of costs to execute dispositions (including $2 million for the sale of HHS which closed in October 2020 and $24 million for the sale of HPS which closed on April 1, 2021); $17 million in expenses related to integration projects resulting from the CSC – HPE ES merger (including costs associated with continuing efforts to separate certain IT systems) and $9 million of costs incurred in connection with activities related to other acquisitions and divestitures.

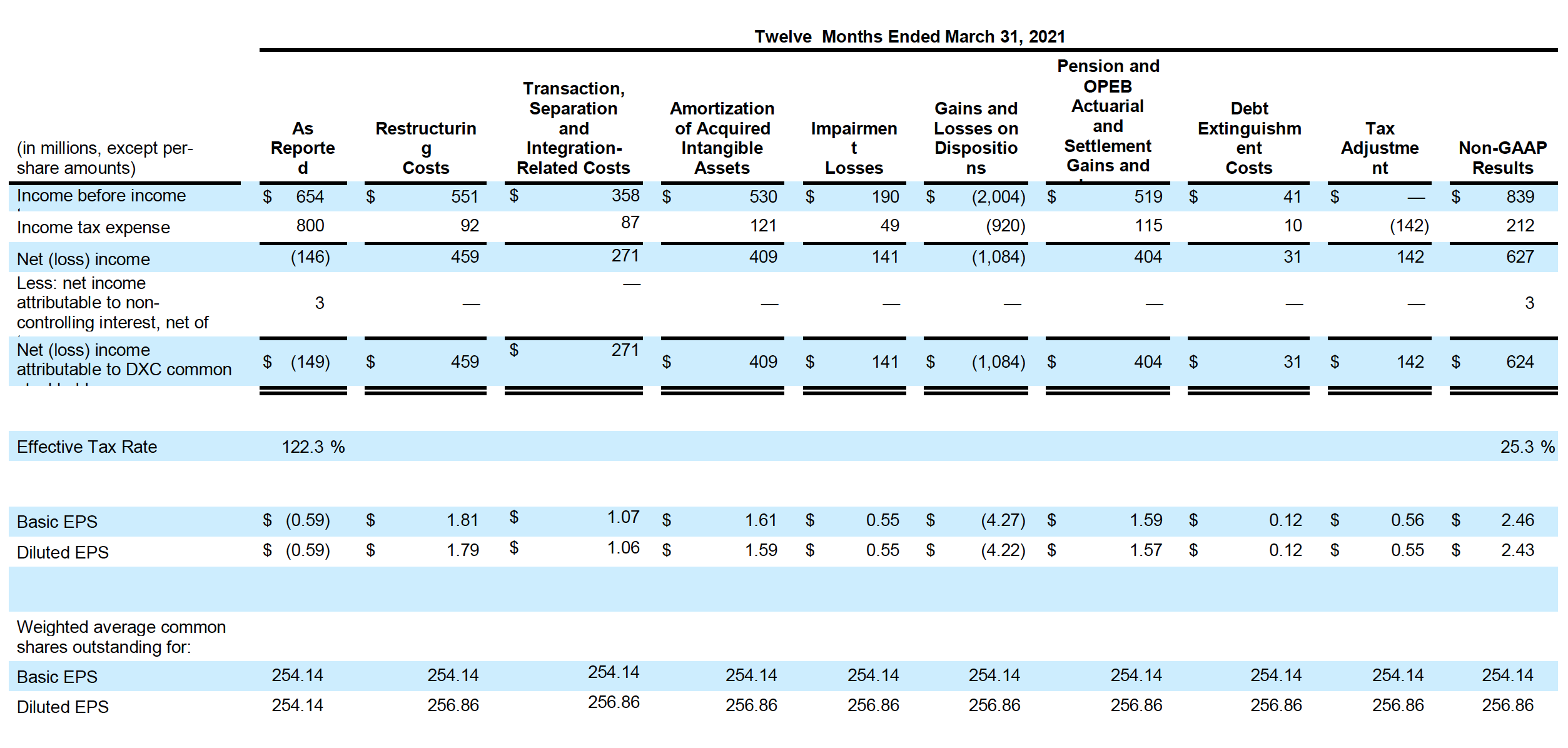

The TSI-Related costs for fiscal 2021 include $250 million of costs to execute dispositions (including $142 million for the sale of HHS which closed in October 2020 and $61 million for the sale of HPS which closed on April 1, 2021); $42 million in expenses related to integration projects resulting from the CSC – HPES merger (including costs associated with continuing efforts to separate certain IT systems) and $66 million of costs incurred in connection with activities related to other acquisitions and divestitures.

(2) Gains and losses on dispositions for the fourth quarter fiscal 2022 includes $(6) million of adjustments relating to the sale of the HPS business and a $4 million gain on insignificant businesses.

Gains and losses on dispositions for fiscal 2022 include a $331 million gain on sale of the HPS business, gains of $23 million on other dispositions and loss of $13 million on adjustments relating to the sale of the HHS business.

Gains and losses on dispositions for the fourth quarter fiscal 2021 includes $27 million of adjustments relating to the sale of the HHS business and a $15 million loss on equity securities without readily determinable fair value, which were adjusted to fair value following receipt of a bona fide offer to purchase.

Gains and losses on dispositions for fiscal 2021 includes a $2,014 million gain on sale of the HHS business, a gain of $5 million on sales of other insignificant businesses, and a $15 million loss on equity securities without readily determinable fair value, which were adjusted to fair value following receipt of a bona fide offer to purchase.

(3) Impairment losses for the fourth quarter of fiscal 2022 of $21 million relate to the impairment of loan receivable and stock warrants associated with a strategic investment.

Impairment losses for fiscal 2022 includes a $10 million impairment charge of capitalized TSI related property and equipment and a $21 million impairment charge of loan receivable and stock warrants associated with a strategic investment.

Impairment losses for the fourth quarter of fiscal 20221 and for fiscal 2021 were $190 million. This includes $165 million impairment for assets pre-purchased through preferred vendor agreements and determined un-deployable, $12 million partial impairment of acquired software, $7 million partial impairment of internally developed software intended for internal use and external sale, and $6 million of capitalized transition and transformation contract costs.

(4) Debt extinguishment costs adjustments for fiscal 2022 includes $18 million to fully redeem two series of our 4.45% senior notes due fiscal 2023, $7 million associated with asset financing, $1 million to fully redeem our Euro-denominated term loan facility, $41 million to fully redeem our 4.25% senior notes due fiscal 2025, $26 million to fully redeem our 2.75% senior notes due fiscal 2025, $58 million to fully redeem our 4.125% senior notes due fiscal 2026, $87 million to fully redeem our 4.750% senior notes due fiscal 2028, $71 million to fully redeem our 7.45% senior notes due fiscal 2030, and $2 million related to the decrease in our revolving credit facility limit.

Debt extinguishment costs adjustments for the fourth quarter of fiscal 2021 and for fiscal 2021 includes $34 million to fully redeem our 4.00% senior notes due fiscal 2024 and $7 million to partially redeem two series of our 4.45% senior notes due fiscal 2023 via tender offer.

(5)Tax adjustment for the fourth quarter of fiscal 2022 includes $32 million for the net revaluation of deferred taxes resulting from changes in non-US jurisdiction tax rates, and $(7) million of adjustment to the transition tax.

Tax adjustment for fiscal 2022 includes $50 million for the net revaluation of deferred taxes resulting from changes in non-US jurisdiction tax rates, and $(7) million of adjustment to the transition tax.

Tax adjustment for fiscal 2021 includes $175 million for the impairment of the German deferred tax asset via a valuation allowance, $9 million for tax expense relating to the U.S. Public Sector business (“USPS”) spin-off, offset by $35 million tax benefit related to the held for sale classification of the Healthcare Provider Software business, and $7 million tax benefit related to prior restructuring charges. The German tax asset was created from multiple periods of losses in Germany that, if not for certain non-GAAP adjustments of restructurings, pension mark to market loss, and impairments, would not have required the asset to be impaired and a valuation allowance established.

The above tables serve to reconcile the Non-GAAP financial measures to the most directly comparable GAAP measures. Please refer to the “About Non-GAAP Measures” section of the press release for further information on the use of these Non-GAAP measures.